Truth in Lending

Read the information below and start the quiz whenever you're ready. You can come back to this page at any time.

Disclosures - "Truth in Lending"

Dealers are required to be compliant with the Motor Vehicle Sales and Finance Act and Code of Federal Regulations "Z" also known as the "Truth in Lending" law.

You must fully disclose all credit terms so Buyers can compare credit terms more easily. You and all creditors must use the same terminology and expressions of rates.

When the Buyer is financing, you must disclose and itemize:

1) The vehicle's cash price alone

2) Any fees charged for:

- Contract Cancellation Option agreement

- Document processing charges

- Debt cancellation agreements

- DMV registration or transfer fees

- Electric vehicle charging stations

- Prior credit or lease balance remaining on trade-in

- Sales tax

- Smog Certification fees

- Service contracts

- Theft-deterrent products

- Surface protection products

3) The total cash price, which is the sum of #1 and #2

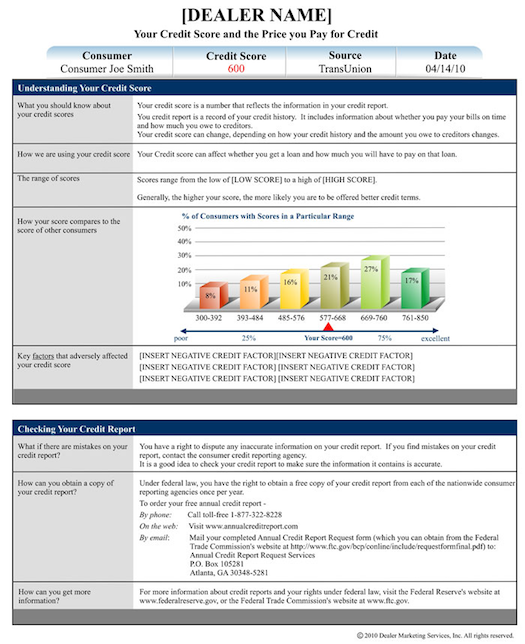

Disclosure of Credit Scores

Click to expand

Dealers are required by the Car Buyer's Bill of Rights (FFVR 35) to provide Buyers with a separate, written "Notice to Vehicle Credit Applicant" in at least 10-point type which discloses:

- Each credit score obtained and used by the dealer

- The date the credit score was created

- The name of the consumer reporting agency for each credit score used by the dealer

- The range of possible credit scores used to generate that credit score

- Statements:

- "A Consumer Report or Credit Report is a record of the consumer's credit history and includes information about whether the consumer pays their obligations on time and the amount owed to creditors"

- "A Credit Score numerical rating is derived from information in a consumer report and can fluctuate over time to reflect changes in the consumer's credit history"

- "Consumer's credit scores may affect whether the Consumer can obtain credit and the cost of that credit"

- The distribution of the consumer credit score, used to generate the same credit score provided to the consumer

- Contact information for the centralized source from which consumers may obtain their free annual consumer reports

Contracts Not Executed & Breach of Contract

If the Contract is not executed, any payment made to you by the Buyer must be refunded.

If the Contract is not executed, any payment made to you by the Buyer must be refunded.

If the Dealer breaches the Contract or Purchase Order after the Buyer leaves his motor vehicle as down payment, you must within 5 days either:

- Return the vehicle to the Buyer

- Pay the Buyer the fair market value of the vehicle or its value as stated in the Contract (whichever is greater)

The Buyer may also pursue remedies under any other provision of law

Defaults on Contracts

There are several reasons where a Buyer may be found in default of the Contract:

- The Buyer or any person liable fails to make any payment due under the contract

- The Buyer fails to keep and maintain the motor vehicle free from all encumbrances and liens of every kind

- The Buyer fails to keep and maintain insurance on the motor vehicle

- The Buyer fails to perform any other obligation under the Contract

Repossessions

If a Buyer defaults on their loan and the Dealer repossesses (or accepts the vehicle back), any person liable on the contract can reinstate the contract.

If a Buyer defaults on their loan and the Dealer repossesses (or accepts the vehicle back), any person liable on the contract can reinstate the contract.

The Dealer or Lender cannot accelerate any part or all of the contract unless they reasonably determine:

1) The Buyer -or- any other person liable on the Contract:

- Intentionally provided false or misleading information of material importance on their credit application -or-

- Committed, attempted, threatened to commit criminal acts of violence or bodily harm against an agent, employee, or officer of the seller or holder in connection with the seller's or holder's repossession of or attempt to repossess the motor vehicle

2) The Buyer -or- any other person liable on the Contract -or- any permissive user:

- Concealed the motor vehicle or removed it from the state to avoid repossession

has committed or threatens to commit acts of destruction, so that the motor vehicle has become substantially impaired in value - Failed to take care of the motor vehicle in a reasonable manner, so that the motor vehicle may become substantially impaired in value.

3) The Buyer has knowingly used the motor vehicle, or has knowingly permitted it to be used, in connection with the commission of a criminal offense, causing the motor vehicle has been seized by a federal, state, or local agency or authority pursuant to federal, state, or local law.

Valuable Reference Links